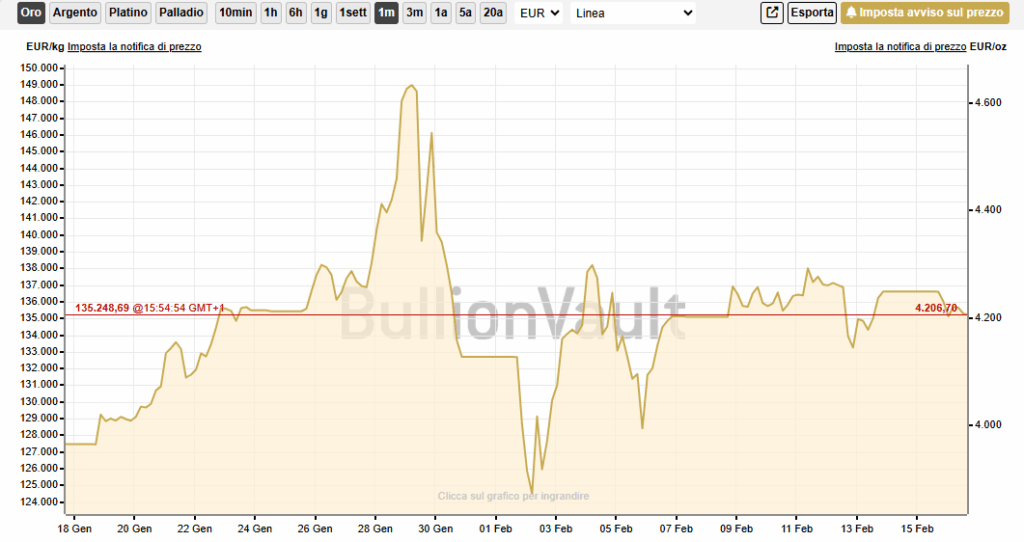

It seemed like the beginning of a record-breaking rally. An incredible €10 per gram surge in a single night, on 29 January 2026. Geopolitical tensions pushed demand for the precious metal sky-high, while the US dollar index fluctuated.

Gold reached historic intraday highs of $5,595–5,600 per ounce, closely followed by silver, which reached $119.67 per ounce (approximately £77.6 per gram).

So, while Trump was talking tough against Iran, threatening repercussions if it did not dismantle its nuclear arsenals, markets around the world were trembling. The regime’s attacks on thousands of protesters on the streets of Tehran sent tensions with the US skyrocketing: the price of crude oil took off, reaching its highest level in six months, and demand for safe-haven assets pushed gold and silver to new records overnight.

However, the euphoria surrounding precious metals was short-lived. By January 30, gold and silver had already lost 10% and 30% respectively ahead of the weekend. This came as no surprise to analysts, who considered the prices reached in the previous hours to be overextended.

This momentum was unsustainable, especially in the first month of the year. Neil Welsh, Head of Metals at Britannia Global Markets, highlighted the incredible volatility of gold and silver on January 29 and 30, describing the retracement as “not surprising, considering the speed and scale of the January rally.” The yellow metal and its “less noble” cousin had gained nearly 20% and over 40% respectively, with positions typical of short-term peaks.

The volatility of the following days was caused by increasingly complex trading conditions, precisely because of the exaggerated rises on 29 January.

The sell-off should therefore not be seen as a crisis in the precious metals market, nor as a loss of confidence in safe-haven assets; rather, it represents a healthy correction, a natural response to the exuberance surrounding gold and silver.

According to analysts, the upward trend has not been damaged by the price retracement at the end of January; on the contrary, the driving forces behind precious metals are still firmly in place and are expected to remain so for the rest of the year. 2026 therefore looks set to be a year full of support for the gold and silver market, albeit with a wider range of fluctuations than in the previous year.

Persistent political and economic uncertainty should prevent the yellow metal from falling further, mainly due to the perennial anxiety in the markets. Fears that an unpredictable political decision could upset the delicate global balance are supporting the upward trend, while the possible decline is estimated at around $4,600 per ounce. However, this threshold will be difficult to reach, given that any price retracement will likely be seen by investors as an opportunity to strengthen their long positions.

The G7’s debt, which is growing beyond already unsustainable levels, and potential inflationary pressures weigh heavily. The US dollar continues to lose popularity, while the need for assets that can preserve their value despite geopolitical turmoil is growing.

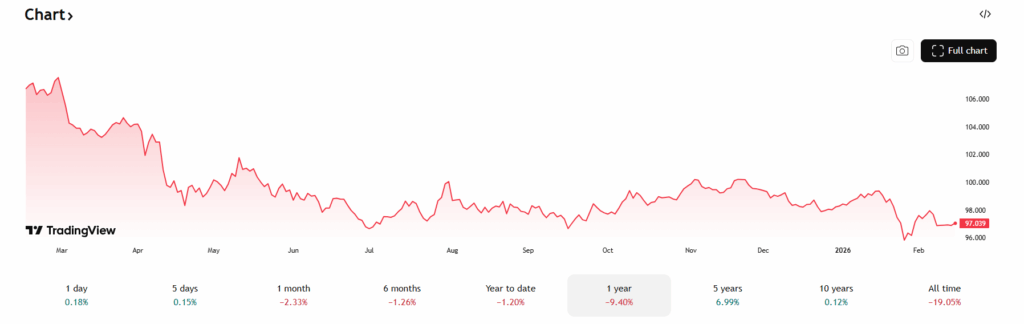

To get an idea of the greenback index trend, simply take a look at the chart below:

In just one year, the US currency has lost 9.03% of its value. This figure reflects a loss of confidence that is difficult to halt, especially in light of weaker-than-expected inflation figures.

Consumer prices in January fell short of expectations, paving the way for the US Federal Reserve (Fed) to make further interest rate cuts during the year.

The Fed unknown: what would change with a new president

2026 could be a year of major changes at the Fed. 15 May marks the end of the term of the current chair, Jerome Powell, who has been repeatedly criticised by Donald Trump, who has accused him of not cutting rates as quickly and aggressively as required. However, as a member of the Board of Governors, Powell could take advantage of his separate term of office to remain in office until 31 January 2028.

Trump would like Powell’s position to be taken over by Kevin Warsh, former governor of the central bank in 2006, who could provide greater stability to the US monetary situation. Although Warsh is known for his restrictive stance on monetary policy, analysts believe it is unlikely that he would go against Trump’s directives: low interest rates to stimulate the economy, despite the risk of inflation just around the corner.

The election of a new president – or the re-election of the incumbent – could play a key role in the performance of precious metals over the coming months: if a hawkish policy remains in place, with interest rates kept high over the long term, the dollar could strengthen at the expense of gold and silver. Conversely, a more accommodative stance in support of economic growth could further weaken the US currency, opening up a new possible runway for precious metals.

Sources

Investing_il dollaro fatica a guadagnare terreno.Lo yen soffre per i deboli dati di crescita.

Euronews_Fed,il bivio di Jerome Powell