More bombs, more winds of war. The Middle East region seems destined not to find peace.

February 28 marked a dramatic turning point in the negotiations between the United States and Iran, after the Western superpower launched a joint operation with Israel on Iranian territory. After an initial wave of market jitters, the strengthening of the U.S. dollar benefited markets, to the detriment of traditional safe-haven assets.

Gold opened the month above $5,400 per ounce (around €148 per gram) — a notable increase compared to the $5,174 recorded on the last day of February (around €140.9 per gram), though still below the all-time high of $5,594.82 reached on January 29 this year.

The peak reached at the beginning of the year (visible in the chart below, which reflects gold’s performance from the start of the year to today) can once again be traced back to tensions between the United States and Iran. Just the day before, U.S. President Donald Trump had raised the tone with Iran, urging it to negotiate a nuclear agreement. Tehran’s response was immediate, threatening retaliation against the United States, Israel, and their allies.

However sudden, the increase on January 29 proved to be more of a flash in the pan than the start of a new rally. Tempted by the high price, many investors liquidated their positions to lock in profits. The following day, gold suffered its largest drop in the past 40 years: more than 12%, reaching a low of $4,682 per ounce.

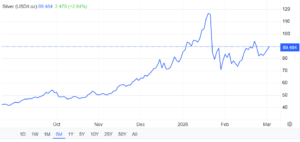

If gold’s contraction was sharp, silver experienced the worst intraday drop in history: a fall of 36%, with prices plunging to $74.28 per ounce.

The entry into the market of that segment of investors waiting for price dips, combined with the escalation of geopolitical tensions, brought prices back to a situation of relative stability at the beginning of February.

Yellow metal little changed: attention now turns to black gold.

The eyes of the world remain fixed on the Strait of Hormuz, the key channel for oil tanker traffic. In the event of disruptions or slowdowns, a scenario of global energy shock could materialize, with a consequent rise in inflation expectations.

About one fifth of the world’s total oil supply passes through the Strait of Hormuz; consequently, any disruption could easily reshape the geopolitical landscape.

Gold began the second week of March down 1%, pressured by a stronger-than-expected U.S. dollar and higher interest rates. Investors are selling their gold positions to secure liquidity, fearing that the war in the Middle East could escalate into a disruption of energy supplies.

There is also little stimulus expected from the U.S. central bank, the Federal Reserve, which during its meeting scheduled for March 17–18 is expected to keep interest rates unchanged.

Silver remains subdued: why war doesn’t benefit the industrial metal.

Even more than gold, the weakness of silver is perhaps surprising. The king of industrial metals and a key player in sectors such as artificial intelligence, mechanical engineering, and photovoltaics—as well as in the military industry—it was perhaps expected to react positively to the mobilization of the war machine.

In reality, the reason behind silver’s lackluster performance lies precisely in the obstacle that war represents for economic growth—and consequently for industrial expansion. Since around half of the demand for physical silver comes from industry, the risk posed to supply chains undermines expectations for future demand. This creates a divergence in prices.

It should also be considered that silver has been the protagonist of unexpected gains over the past two years: +150% in 2025 alone, with new all-time highs already reached at the beginning of this year. Such a performance is prompting investors to pause before buying the white metal, waiting for stronger catalysts. Profit-taking is also clearly playing a role, which is inevitable when prices rise so sharply over such a short period of time (see chart).

Consequently, gold and silver are likely standing at two opposite ends of a crossroads. If geopolitical tensions intensify, gold will probably continue to outperform. Conversely, if economic growth stabilizes and industrial demand regains momentum, silver— a market that has been in a supply deficit for years—could return to posting gains at a sustained pace.

The white metal is characterized by greater volatility than its more “noble” counterpart; for this reason, the growth of these commodities does not move in lockstep.

According to Prathamesh Mallya, Vice President of Research for Non-Agri Commodities at Angel One Ltd, an ideal portfolio would include about 60% gold and 40% silver. Diversification, it should be remembered, allows investors to protect their capital against a broader range of risks.

2026: what outlook for gold and silver?

The conflict between the United States and Iran has brought the greenback back into the spotlight. The U.S. dollar index is near its highest level of the past three months, as investors have turned to the American currency as a safe-haven asset. A strong dollar and expectations of higher Federal Reserve interest rates over the long term reduce the attractiveness of non-yielding assets such as gold and silver.

For this reason, precious metals are struggling to deliver significant performance.

The factors that supported gold prices in 2025 remain in place in 2026 as well—although it must be said that a performance like last year’s will be difficult to replicate. Demand for the metal from central banks is expected to remain stable, confirming the ongoing trend of diversification away from the U.S. dollar. Financial institutions currently hold about 20% of all the gold ever mined, and the increase in their gold reserves remained steady from 2022 to 2025.

A survey conducted last year found that 95% of central banks expect global gold reserves to increase in 2025 (the same survey in 2024 put expectations at 81%, while in 2021 they stood at just 52%).

It should also be noted that emerging superpowers such as China and Brazil still allocate less than 10% of their reserves to gold; consequently, they represent enormous potential support for future demand.

As for private investors, wealth allocations to gold are about 50% lower than they were ten years ago. Private purchases are currently driven mainly by India and China, which together account for nearly 60% of global consumer gold demand. North America and Europe together represent only 15%, highlighting the significant room Western investors still have to increase their allocations.

Finally, new emerging buyers are worth noting in the gold market, among which Tether stands out—the world’s largest stablecoin issuer—which, with its 140 tonnes of gold, currently represents the 33rd largest reserve globally.

The outlook is also positive for silver, which continues to be the reference metal for rapidly growing industrial sectors (from solar panels to data centers, from mechanical engineering to artificial intelligence). Emerging technologies—conflicts permitting—should therefore support significantly higher silver consumption throughout 2026.

In 2024, photovoltaic technology accounted for nearly 29% of total silver demand—a significant figure compared with 11% in 2014. The photovoltaic sector is expected to continue supporting silver demand through 2030.

In the short to medium term, the direction of prices will depend primarily on how the conflict evolves.

Sources:

Gold’s seven-month run meets geopolitical tension in March

Why are gold prices rising but silver falling amid US-Iran war? Explained

Gold slips on stronger dollar, higher rate expectations

Gold and silver: Price, market volatility, and what is next